Hi, this is a comment. To get started with moderating, editing, and deleting comments, please visit the Comments screen in…

The Critical

Materials & Rare Earths Supply Chain: A Complete Analysis

The engine of modern technology-from electric vehicles to advanced

defense systems is fueled by the critical materials

The engine of modern technology-from electric vehicles to advanced defense systems is fueled by the critical materials rare earths supply chain, a global network defined by opacity and extreme geopolitical risk. For strategists and operators, this translates into a constant state of uncertainty: crippling price volatility, the persistent threat of disruption, and the challenge of navigating inefficient processing methods. Reacting to shortages is no longer a viable strategy; proactive, predictive intelligence is the new imperative.

This definitive guide provides that intelligence. We deconstruct the entire supply chain, from mine to magnet, to give you unprecedented visibility. We will illuminate the hidden choke points and systemic vulnerabilities that create risk and explore how next-generation technology, like AI, is forging a new era of resilience. Prepare to move beyond fear of disruption and gain the actionable strategies needed to secure your supply, predict market shifts, and build a definitive competitive advantage.

Defining the Stakes: What Are Critical Materials and Rare Earth Elements?

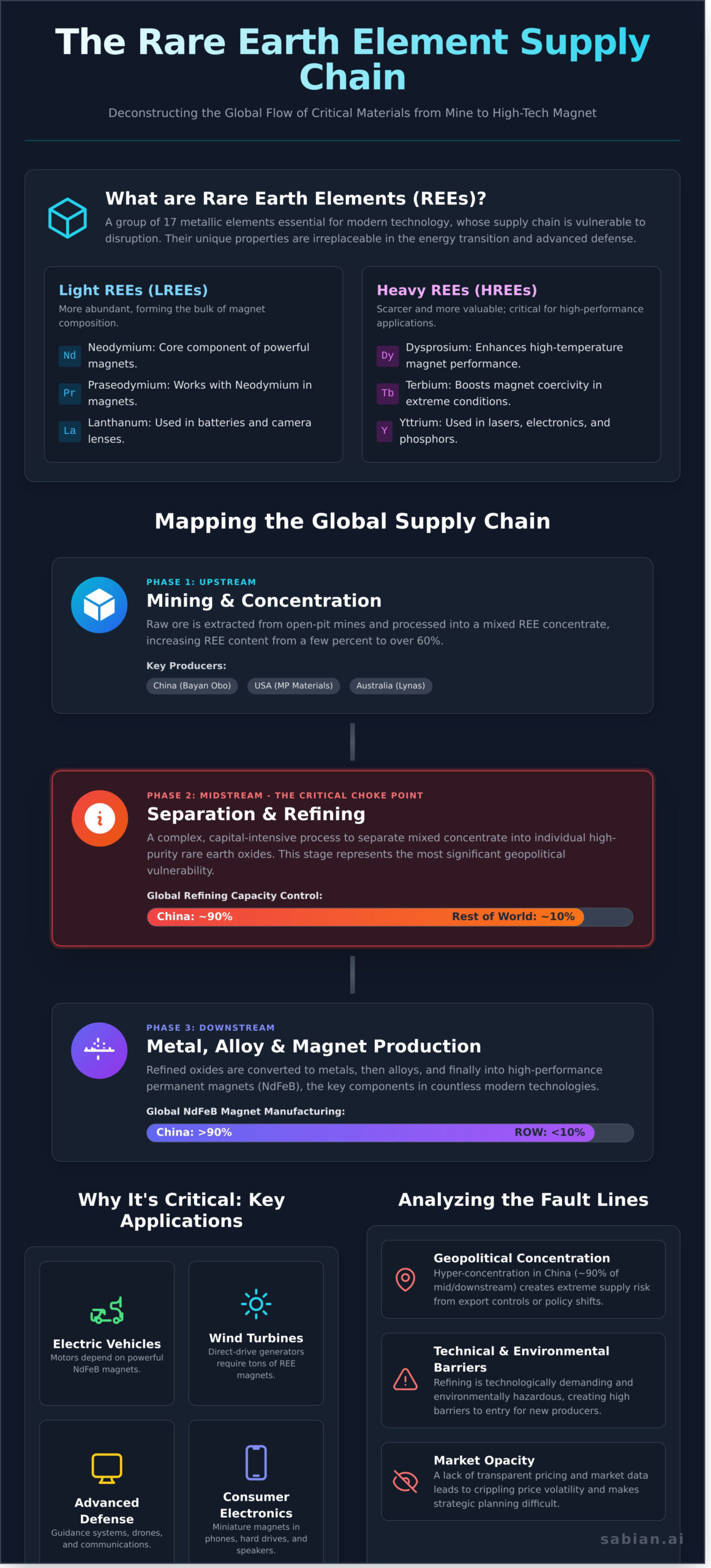

A "critical material," as designated by government bodies like the United States Geological Survey (USGS), is a non-fuel mineral essential to economic and national security whose supply is vulnerable to disruption. Securing this flow of resources is the central challenge for the entire critical materials rare earths supply chain. Within this vital category, a specific group commands immense strategic importance: the 17 metallic elements known as the rare earth elements (REEs). Their properties are irreplaceable in modern technology, forming the foundation of the global energy transition and advanced defense platforms.

Despite their name, REEs are not geologically rare. The paradox lies in their dispersal; they are seldom found in concentrations high enough for economic extraction, making commercially viable deposits a strategic global asset. This processing challenge is a core vulnerability in the critical materials rare earths supply chain.

-

Scandium (Sc)

-

Yttrium (Y)

-

Lanthanum (La)

-

Cerium (Ce)

-

Praseodymium (Pr)

-

Neodymium (Nd)

-

Promethium (Pm)

-

Samarium (Sm)

-

Europium (Eu)

-

Gadolinium (Gd)

-

Terbium (Tb)

-

Dysprosium (Dy)

-

Holmium (Ho)

-

Erbium (Er)

-

Thulium (Tm)

-

Ytterbium (Yb)

-

Lutetium (Lu)

Why ‘Critical’? The Link to Economic and National Security

The strategic value of REEs is encoded in their unique atomic properties. Elements like Neodymium (Nd) and Praseodymium (Pr) are fundamental to creating the world’s most powerful permanent magnets-the core components driving electric vehicles and wind turbines. Others, such as Yttrium (Y) and Europium (Eu), are indispensable for advanced electronics and phosphors. The conclusion is stark: without a resilient critical materials rare earths supply chain, the production of next-generation technology is fundamentally compromised. This reality is reflected in their prominent placement on official critical mineral lists maintained by the United States and the European Union.

Light vs. Heavy Rare Earths (LREE vs. HREE)

REEs are categorized into Light Rare Earths (LREEs) and Heavy Rare Earths (HREEs). This is not just a scientific distinction; it is a critical variable that introduces significant risk into the critical materials rare earths supply chain. HREEs, such as Dysprosium (Dy) and Terbium (Tb), are significantly scarcer and more valuable. Their primary function is to enhance the performance of magnets, allowing them to operate effectively under extreme temperatures-a non-negotiable requirement for advanced military hardware and high-performance industrial motors. This scarcity makes HREEs a key point of vulnerability, putting immense pressure on an already stressed critical materials rare earths supply chain.

Mapping the Global Supply Chain: From Mine to High-Tech Component

Understanding the vulnerabilities within the critical materials rare earths supply chain requires a clear map of its structure. The journey from raw ore to a finished high-tech component is a linear, multi-stage process characterized by extreme geographic concentration. This value chain can be deconstructed into three distinct phases: Upstream, Midstream, and Downstream.

Upstream: Mining and Concentration

The supply chain begins with Upstream extraction. Rare Earth Elements (REEs) are typically mined from large-scale open-pit operations, where raw ore is blasted and excavated. This ore then undergoes initial processing-crushing, grinding, and flotation-to produce a mixed rare earth concentrate, increasing the REE content from a few percent to over 60%. While China’s Bayan Obo mine remains a dominant source, mining operations are becoming more geographically diverse, with significant production from facilities like MP Materials in the United States and Lynas Rare Earths in Australia.

Midstream: The Critical Choke Point of Separation and Refining

The Midstream stage is the most significant bottleneck in the entire system. Here, the mixed concentrate undergoes a highly complex and chemically intensive solvent extraction process to separate the 17 individual rare earth elements into high-purity oxides. This is a technologically demanding and environmentally challenging phase that requires immense technical expertise. China overwhelmingly dominates this stage, controlling approximately 90% of global refining capacity. This hyper concentration creates significant geopolitical vulnerabilities in the supply chain, as national industrial policy or export controls can disrupt the global flow of these essential materials.

Downstream: Metal, Alloy, and Magnet Production

In the final, Downstream stage, the refined rare earth oxides are converted into metals, which are then mixed to form specialized alloys. The most crucial output of this stage is the production of high-performance neodymium iron boron (NdFeB) permanent magnets. These powerful, lightweight magnets are indispensable components for electric vehicle motors, wind turbines, defense systems, and consumer electronics. Mirroring the midstream, this segment is also heavily concentrated, with China manufacturing over 90% of the world’s NdFeB magnets, directly linking this industrial dominance to the world’s most critical technology sectors.

Analyzing the Fault Lines: Key Vulnerabilities in the REE Supply Chain

The structural fragility of the global rare earth element (REE) supply chain is not a singular point of failure but a complex network of interconnected risks. These vulnerabilities, synthesized from intelligence by agencies like the IEA and GAO, expose Western economies to significant disruption. The Department of Energy’s analysis of the rare earths supply chain confirms that these fault lines can be categorized into three primary domains: geopolitical concentration, technical and environmental barriers, and severe market opacity.

Geopolitical Concentration and Weaponization

The most acute vulnerability stems from extreme geographic concentration. China currently controls an estimated 85-90% of global REE refining and processing capacity the critical midstream stage where raw ores are converted into high-purity oxides and metals. This dominance has been leveraged as a tool of statecraft, with export controls on materials like gallium and germanium serving as a recent reminder of this power. For industries reliant on high-performance magnets-from F-35 fighter jets and guided missile systems to EV motors and wind turbines-this dependency represents a direct threat to national and economic security. Understand how geopolitical risk impacts mineral supply.

Technical, Environmental, and ESG Hurdles

Replicating the midstream processing infrastructure outside of dominant nations is a monumental challenge. Building new separation and refining facilities is not only capital intensive, requiring billions in investment, but also technically complex. Furthermore, traditional REE processing generates significant environmental liabilities, including radioactive tailings. In an era of heightened regulatory scrutiny and investor pressure for high Environmental, Social, and Governance (ESG) standards, these legacy issues create a formidable barrier to entry for new producers in North America and Europe, slowing the diversification of the critical materials rare earths supply chain.

Price Volatility and Opaque Market Dynamics

Unlike commodities such as copper or gold, which trade on transparent, centralized exchanges, the REE market is notoriously opaque. Pricing is dictated by a small number of dominant state-influenced players, leading to extreme price volatility and a lack of forward visibility. This market structure creates immense uncertainty for end-users and project developers alike. It complicates long-term offtake agreements, deters institutional investment in new mining and refining projects, and makes it nearly impossible for manufacturers to forecast costs, thereby stifling innovation and resilience.

Building Resilience: Strategies to Secure Future Supply

Identifying vulnerabilities is the first step; building resilience is the strategic imperative. A secure supply of critical materials is not achieved through a single solution but through a multi-faceted strategy. The path forward combines geopolitical diversification, technological innovation, and a foundational layer of predictive intelligence to fortify the entire value chain.

Diversification: The ‘Friend-Shoring’ and Onshoring Imperative

Reducing dependency on any single state actor is paramount. Western governments are aggressively promoting this shift through policies like the Inflation Reduction Act, which incentivizes domestic production and processing. This has catalyzed new ex-China refining capacity projects in the United States, Australia, and Canada. These onshoring efforts, combined with ‘friend-shoring’-building robust supply networks with strategic allies are creating a more distributed and shock-resistant ecosystem. Success, however, depends on navigating the significant challenges of onshoring REE processing.

Innovation: Recycling and Alternative Technologies

Beyond geographic diversification, innovation offers two powerful levers: creating new supply streams and designing out dependencies. This includes:

-

Urban Mining: End-of-life electronics, from smartphones to wind turbines, represent a vast, untapped reservoir of critical minerals. Advanced recycling technologies are making it possible to reclaim these elements efficiently.

-

Circular Supply Chains: The ‘black mass’ derived from recycled EV batteries is becoming a key secondary source for lithium, cobalt, and nickel, closing the loop on a resource-intensive process.

-

Material Science: Research is accelerating into alternative magnet technologies that reduce or eliminate the need for specific rare earth elements, fundamentally altering future demand.

Fortification: The Rise of Predictive Intelligence

You cannot manage what you cannot measure. Traditional management is reactive, responding to disruptions after they occur. Fortifying the modern critical materials rare earths supply chain requires a paradigm shift to proactive, predictive intelligence. This means leveraging real time data and advanced analytics to anticipate bottlenecks, model geopolitical risk, and identify optimization opportunities. Intelligence is the enabling layer that makes diversification and innovation strategies truly effective. Harnessing this foresight, as pioneered by platforms like AI for Critical Minerals, transforms uncertainty into a strategic advantage, setting the stage for the next leap in supply chain security.

The AI Advantage: Fortifying the Supply Chain with Predictive Intelligence

Addressing the systemic fragilities within the global minerals network requires a paradigm shift from reactive problem solving to proactive, data driven strategy. Predictive intelligence, powered by artificial intelligence, offers the necessary tools to transform operational efficiency and strategic foresight. By leveraging AI, stakeholders can move beyond historical analysis and begin to accurately model future states, de-risking the entire value chain from extraction to end-use.

Optimizing Production and De-risking the Midstream

The technical complexities of mineral processing represent a significant vulnerability. AI directly mitigates these operational risks by introducing a new level of precision and predictive capability. Machine learning models can analyze and stabilize the notoriously volatile chemistry of solvent extraction and other refining processes, maximizing purity and yield. This intelligence extends to physical assets, where AI enables:

-

Predictive Maintenance: Algorithms analyze sensor data from mining and refining equipment to forecast failures before they occur, drastically reducing costly unplanned downtime.

-

Geometallurgical Optimization: AI models process complex geological data to predict metallurgical performance, allowing for optimized ore blending and processing strategies that increase mineral recovery from the same deposit.

Creating End-to-End Visibility and Forecasting

The opacity of the critical materials rare earths supply chain has long been a primary source of risk. AI driven platforms dismantle these information silos by integrating disparate data sources-from satellite imagery and geological surveys to real-time market pricing and geopolitical risk indicators-into a single, holistic intelligence layer. This unified view powers predictive analytics that can forecast supply bottlenecks, demand surges, and price fluctuations with unprecedented accuracy. This capability allows organizations to anticipate disruptions and strategically adjust procurement, inventory, and production schedules, transforming volatility into a manageable variable. See how PREDICTUS mitigates supply chain volatility with AI.

By embedding predictive intelligence into its core, the critical materials rare earths supply chain can evolve into a resilient, efficient, and secure ecosystem. The technology to build this future exists, offering a definitive strategic advantage to the organizations that embrace it. Learn more about the future of mineral intelligence at sabian.ai.

The Future of Supply Chain Resilience is Predictive

The analysis is clear: the vulnerabilities embedded within the global network for rare earths and critical materials pose a significant threat to industrial and economic stability. While traditional strategies like diversification are essential, they are no longer sufficient to navigate accelerating complexity. The path forward demands a paradigm shift from reactive mitigation to proactive, predictive intelligence.

Mastering the modern critical materials rare earths supply chain requires foresight. Sabian.ai delivers this advantage. As the world’s first AI platform for critical minerals, we empower producers, governments, and buyers by transforming complex plant data into decisive operational foresight. We provide the intelligence to anticipate disruption, optimize production, and secure your position in the new global economy.

Secure your advantage. Request a consultation to gain predictive intelligence on your supply chain and begin building a more resilient future.

Frequently Asked Questions

What is China’s current market share in the rare earths supply chain?

China exercises dominant control over the global rare earth element (REE) supply chain. While its share of mining has decreased to approximately 60%, it commands over 85% of the global capacity for processing and refining REEs into the high-purity oxides and metals required for advanced manufacturing. This strategic concentration gives Beijing significant geopolitical and economic leverage, creating vulnerabilities for nations dependent on these critical inputs for their defense, energy, and technology sectors.

Is recycling a viable short-term solution to REE supply concentration?

Recycling is a critical long-term strategy but not a viable short term solution for diversifying the REE supply. The current volume of end-of-life products containing significant REEs, such as permanent magnets from EVs and wind turbines, is insufficient to meet escalating demand. Furthermore, the technological and economic challenges of efficiently separating and refining these elements from complex alloys remain substantial. Investment in recycling technology is essential, but new primary sources are the immediate imperative.

How do government policies like the Inflation Reduction Act impact the REE supply chain?

Policies like the U.S. Inflation Reduction Act (IRA) are designed to fundamentally reconfigure the critical materials rare earths supply chain. By offering substantial tax credits for electric vehicles (EVs) that source batteries and critical minerals from North America or allied nations, the IRA creates powerful financial incentives for automakers to divest from Chinese suppliers. This demand-side stimulus is accelerating investment into domestic mining, processing, and recycling facilities, directly challenging existing market concentration.

What are the biggest environmental challenges in rare earth processing?

The primary environmental challenges in rare earth processing stem from the chemical intensive separation stage. Extracting individual REEs from ore requires vast quantities of strong acids and other hazardous chemicals, generating significant toxic waste, or tailings. Furthermore, many rare earth deposits co-locate with radioactive elements like thorium and uranium. Managing and safely disposing of these low level radioactive byproducts represents a major technical, regulatory, and long term environmental liability for any processing operation.

Can rare earth elements be substituted in applications like EV motors?

Substitution is technologically possible but involves significant performance trade offs. High-performance permanent magnet motors, which rely on neodymium and praseodymium (NdPr), offer the best power density and efficiency for EVs. While alternatives like induction motors or ferrite based magnets exist, they are typically heavier, larger, and less efficient, which can negatively impact vehicle range and performance. Intensive R&D is focused on developing high-performance, magnet free motor technologies to mitigate supply risk.

How long does it take to build a new rare earth mine and refinery?

Developing a new rare earth mine and refinery is a capital-intensive process, typically requiring 10 to 15 years from discovery to full production. The timeline includes several years for geological exploration and feasibility studies, followed by a lengthy and complex permitting phase which can last 7-10 years in Western jurisdictions. Construction of the mine and the highly specialized processing facility can then take an additional 2-4 years, representing a significant barrier to rapid supply chain diversification.